Private Equity

May 21, 2021

What is “Private Equity”?

Private equity refers to ownership capital, comprised of funds or investors, which is invested in start-up, growing, or established companies that are not listed on a public exchange. A private equity investment in a public company can result in the company becoming private if a majority stake is acquired, which is often the case in a leveraged buyout or LBO. Private equity investments are typically made through the use of funds, which are raised by private equity firms and invested in by sophisticated investors.

Key Learning Points

- Private equity is ownership capital in companies or assets that are not (or no longer) publicly listed

- In addition to investing their own capital, private equity firms raise capital through funds using outside investors

- Private equity is used to finance start-up (venture), growth, mature and distressed companies

- Many of these investments involve complicated and risky transactions such as LBOs, which use high levels of debt to acquire a company to drive growth or performance improvements

- The riskiness of private equity combined with the lack of liquidity of the investments contribute to the high targeted returns of 20% and up

An Overview

Private equity is an alternative investment class and PE firms seek elevated returns from opportunities and advantages in private markets that do not typically exist in the more efficient public markets. Most investments are not entirely passive but rather, made for the purpose of actively managing an investment to improve returns.

The downside of this type of investment can be the lack of liquidity or the ability to sell on short notice which is a hallmark of the public markets. As a result, private equity investments tend to adopt hold strategies of three to five years. Private equity can be both preferred or common and is often a combination of both.

The investment vehicle for this ownership capital are funds that represent a partnership between the private equity firm (the general partner or GP), which invests its own capital alongside limited partners (or LPs). Limited partners are comprised of wealthy individuals, sovereign wealth investors, pension funds, and other institutions. There is usually a fee for fund management and then also a percentage ‘bonus’ of the ultimate return paid back to the fund managers, or private equity firm. Funds typically have an expected duration at which time they are liquidated to return cash to the investors.

Investment Targets

Private equity can be used to fund any asset class. Traditionally, private equity has been directed most frequently at corporations. There are several types of companies that make good targets for investment:

- Startup or Venture Capital: these investments tend to come in the early stages of finance after the company has already attracted some initial investment and has proven a viable concept.

- Growth: many companies looking to expand by acquisition or asset development will seek private equity investment (alongside debt) to fund this growth.

- Distressed: since active investment is a component of private equity, firms will look for companies with positive outlooks in need of turnaround strategies. In these cases, private equity will work closely with management or install new management to instigate the desired changes.

- Complex transactions: in many of the above situations, private equity firms will bring financial expertise to deals to arrange the best possible capital structure and set the company up for the highest return on investment. These strategies often involve transactions such as leveraged buyouts or LBOs that use significant levels of debt and minimal equity. By using debt (which is secured by the company’s assets) to finance the company’s turnaround or growth, the residual private equity value can grow in value at very high rates of return.

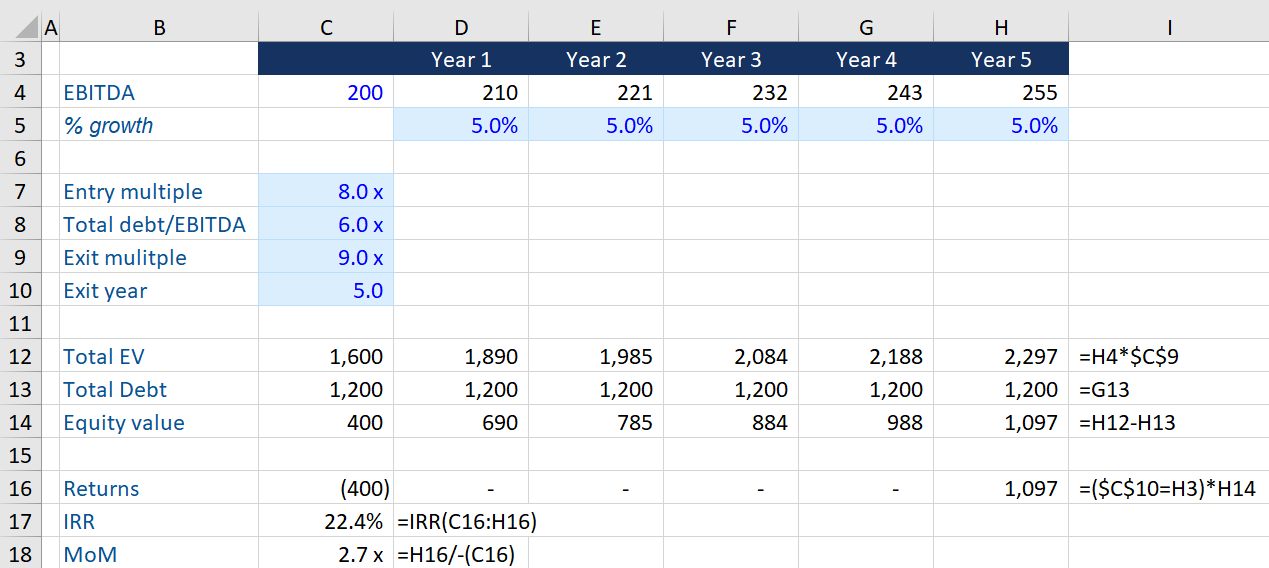

Targeted Returns

Historically, private equity target returns have been 20% and higher, typically measured by the IRR. This elevated rate is due to the perceived riskiness and illiquidity of the investments. The major factors affecting the returns are the price paid, the amount of equity required to close the deal, the length of the holding period, the performance of the company, and the selling price. As competition for assets has increased, achieving acceptable returns has become much more challenging forcing private equity to consider more ways to bolster returns.

Another common way to measure private equity performance is through the metric “multiple of capital invested” (this is more commonly called “multiple of money” or “cash on cash”). This is simply the ratio of the equity value at sale over the equity value invested, irrespective of time.

Conclusion

Private equity seeks to exploit market inefficiencies between public and private enterprises. In theory, without public markets, private corporations are less efficiently priced leaving opportunities to generate higher returns than in the public markets.

Take our private equity course that is designed by five industry experts who share 14 years of experience in private equity and leveraged finance.