Correlation and Covariance Workout

Sign up to access your free download and get new article notifications, exclusive offers and more.

Correlation and Covariance

April 29, 2022

What are Correlation and Covariance?

Correlation and covariance are statistical tools that measure the relationship between two variables, and they play a vital role in the field of finance. Correlation measures the degree to which two variables move in sync with each other. If they move in the same direction, then the two variables are positively correlated. If they move in opposite directions, they are negatively correlated. The correlation coefficient lies between -1 and +1 and indicates the strength and direction of the relationship between two variables. It is a pure value and not measured in any type of units.

Covariance indicates only the direction of the linear relationship between two variables, not the strength of the relationship between the two. A positive (negative) covariance indicates that the two variables move together in the same (opposite) direction. Covariance is central to the concept of correlation between two variables, as correlation is calculated by dividing the covariance between two variables by the product of their standard deviations. Covariance is used in portfolio theory to determine what assets should be included in a portfolio to maximize diversification.

Key Learning Points

- Correlation is often used to measure how strongly a stock moves in relation to a benchmark index, for example, the S&P 500.

- Covariance is central to the concept of correlation between two variables, as correlation is calculated by dividing the covariance between two variables by the product of their standard deviations.

- In portfolio management, correlation helps to measure the level of diversification afforded by the combination of assets included in a portfolio.

- To gain an insight into the pivotal role that covariance and correlation play in investment decisions, we focus on a key parameter – Beta.

- Beta is used to determine the volatility of an asset or portfolio relative to that of the overall market.

- To calculate beta, we need to know the covariance between the return on the stock/fund/portfolio and the return of the overall market, along with the variance of market returns.

Formula

Calculate correlation and covariance using the following formulas:

Correlation = cov(X,Y)/St. Dev. (x), St.Dev (y)

Where:

Cov(X,Y) = Covariance between X and Y

Cov (X,Y) = E(X – E(X)) (Y – E(Y))

If two variables X and Y have expected values E(X) and E(Y), then we can calculate the covariance between the two variables using this formula.

St. Dev. (x) = Standard deviation of X

St. Dev. (y) = Standard deviation of Y

This equation states that the correlation between two variables, X and Y, is the covariance between X and Y divided by the product of the standard deviations of these two variables. Further, this formula shows whether the two variables are positively or negatively correlated, and the degree to which both variables move together or in the opposite direction. The correlation value lies between -1 and +1 and indicates the strength and direction of the relationship. A correlation beyond –0.6 or + 0.6 is generally viewed as a strong negative or positive correlation. If the correlation coefficient is zero, then the two variables have no linear relationship.

On the other hand, if the correlation coefficient is 1, this indicates that the variables are perfectly correlated and move in lockstep. In this case, if one stock moves up or down, the other stock moves exactly in tandem. Correlation is used to measure how a stock moves in relation to a benchmark index. For example, large-cap mutual funds typically have a very strong positive correlation to the S&P 500, often close to 1. Small-cap stocks are also positively correlated with the S&P 500, although to a lesser degree of around 0.8.

In portfolio management, correlation is the basis upon which diversification is achieved in a portfolio. The objective is to diversify away from the stock-specific risk. This is achieved by choosing investments that have a low correlation with each other.

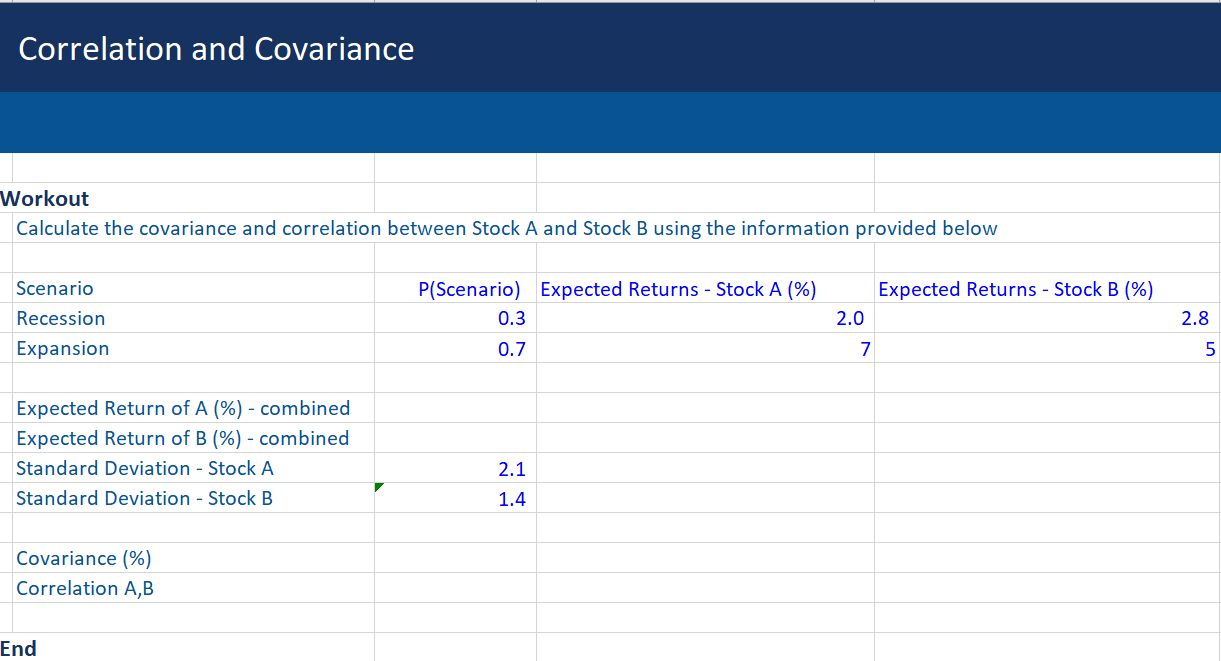

Example

Below is an example in which the correlation and covariance between stocks A and B have been calculated in two scenarios – an economic recession and expansion. We use the formulas mentioned above to calculate the two values. The results show that the covariance between the two stocks, A and B, is 2.3 and the correlation between the two is positive and strong (0.79). The two stocks tend to move in the same direction.

Investments – Correlation and Covariance

In looking at a mutual fund, the investor needs to analyze performance based on certain parameters – average return, standard deviation, Beta (which includes covariance in the formula), correlation, and beta correlation. To determine whether the fund is a good investment, it’s necessary to estimate future returns.

Of these parameters, we focus on Beta to gain an insight into the pivotal role that covariance and correlation play in investment-related decisions.

Beta is used to determine the volatility of an asset or portfolio relative to the overall market. The overall market has a beta of 1 and the riskiness of an individual stock or portfolio is indicated by its volatility in relation to the market. For example, a stock with a Beta of 1.5 is more volatile than the overall market and therefore riskier, while a stock with a Beta of .5 is less risky than the overall market.

In order to calculate beta, it’s necessary to know the covariance between the return on the stock/fund/portfolio and the return of the overall market, along with the variance of market returns.

Beta Formula

Beta = Covariance/ Variance

It’s possible to calculate beta by dividing the stock’s standard deviation by the benchmark’s standard deviation and multiplying this value by the correlation.

Assume that the correlation between Stock A and the S&P 500 is 0.77. Further, assume that the stock has a standard deviation of 20%, while the benchmark stock market index has a standard deviation of 32%.

Beta of Stock A = 0.77 * (0.20/0.32) = 0.481

The calculation reveals that Stock A is much less volatile than the overall market, as it has a beta of 0.481. This suggests that the stock experiences 52% less volatility than the benchmark market index.

Conclusion

The concept of correlation plays an important role within the realm of finance. It’s used to forecast future trends and manage portfolio risk. For example, a fund manager could reduce portfolio risk by selecting assets that are not strongly correlated with each other. Investors can also use historical correlation data to forecast whether a company’s stock price will rise or fall when interest rates change or when there is a change in commodity prices. Moreover, correlation is also used in pricing complex instruments such as derivatives. It’s also possible to reduce portfolio risk by investing in assets that have a negative covariance.

Solve the Following Question on Correlation and Covariance

Below is a question to test your knowledge, download the Excel exercise sheet attached to find a full explanation of the correct answer.