Test Yourself

Sign up to access your free download and get new article notifications, exclusive offers and more.

Investment Grade

May 19, 2021

What is “Investment Grade”?

‘Investment grade’ is a rating awarded to bonds by credit agencies to show its overall creditworthiness and risk assessment. The alternative to investment grade is non-investment grade. Corporate bonds generally promise timely payment of interest and principal or a fixed flow of income, but they cannot be deemed risk-free so they are assigned grades of creditworthiness. This is because the issuers of corporate bonds, typically large corporations, may default on their payment obligations so these payments cannot be 100% certain or guaranteed. The ability of a company to actually make timely bond payments depends to some extent on its ultimate financial position.

The risk that an issuer of a bond will default on its payment obligations is termed as ‘default risk’, or commonly known as ‘credit risk’. To assess the risk of default by the issuer, credit rating agencies, such as Moody’s, Standard & Poor, and Fitch, assign credit ratings to bonds of corporations, which range from AAA (highest quality vis-a-vis credit quality) to D ( in default).

Investment grade bonds are those bonds that are assigned ratings between AAA (highest investment grade) and BBB – or Baa3 (lowest investment grade) – depending on which credit rating agency is rating these bonds.

Essentially, bonds that are believed to have a lower risk of defaulting on their payment obligations are assigned higher credit ratings (e.g. AAA or AA). Investment grade bonds do not usually default. However, they are not free from credit or default risk.

Key Learning Points

- Large corporations tend to regularly issue bonds for varied purposes. The corporate bond market can be divided into four categories detailed below (including investment grade bonds)

- A bond rated “AAA” is judged as offering the highest safety to bond holders vis-a-vis timely payment of interest and principal. There are other sub-categories of investment grade bonds too

- Investment grade bonds tend to be issued at lower yields, when compared to non-investment grade, speculative grade or junk bonds as they can attract investors without needing to offer high yields

- Even though rating agencies have their own rating methodologies, they all undertake two types of analysis – industry and business, and financial analysis for the purpose of rating bonds of issuers (i.e. credit rating)

- The yield to maturity is the rate of return from holding a bond to maturity (for example 20 years), if there is no default and all payments are made as promised.

- When bond prices fall (rise), yield (i.e. yield to maturity) rises (falls)

Investment Grade Bonds – Types of Ratings and related Analysis

Large corporations tend to regularly issue bonds for purposes such as undertaking major capital expenditures, retiring existing debt, or for acquisitions. The corporate bond market can be divided into the following categories: commercial paper, investment grade bonds, high yield bonds (i.e. below investment grade) and leveraged loans.

With reference to investment grade bonds, taking the example of Standard & Poor’s credit rating. if a bond is rated “AAA” (i.e. highest quality), this refers to the highest safety and implies that the issuer’s capacity for payment of interest and repayment of principal is very strong (i.e. lowest risk of default).

An investment grade bond with a credit rating “AA” (i.e. excellent) also has a very strong ability for payment of interest and repayment of principal on time. An investment grade bond with a credit rating of “AA” differs only marginally vis-a-vis safety of payment from “AAA” investment grade bonds.

An investment grade bond, rated at “A” (i.e. good), also has a strong ability or capacity to honor debt obligations and offer adequate safety of payment. However, compared to bonds in the higher investment grade category, they are more susceptible to changing economic conditions and change in circumstances.

An Investment grade bond, rated at “BBB” (i.e. moderate safety – the lowest investment grade), is considered less safer than the other three aforesaid categories and are judged to offer adequate safety vis-a-vis timely payment of interest and repayment of principal. However, changing circumstances, an economic downturn or negative economic conditions are more likely to lead to a lower or weaker capacity to honor bond payment obligations – when compared to bonds in the other three higher investment grade categories.

A company should be concerned, if the rating of its bond falls below BBB (which is the lowest investment grade rating), as it is usually received negatively by the market and results in selling of the bond and consequent fall in the price.

Investment grade bonds are essentially bonds that have a maturity between three to 30 years Most of these bonds have fixed, rather than floating rates. A few 3 and 5 year investment grade bonds have floating rates.

The level and underlying trend of financial ratios of the companies that issue bonds have an important influence on the credit rating of their bonds. These financial ratios are leverage, liquidity, coverage, profitability and cash flow to debt ratios. Rating agencies tend to predicate their ratings of bonds (i.e. their credit rating) largely on the analysis of these ratios.

Even though rating agencies have their own rating methodologies, they all undertake two types of analysis – industry and business, and financial analysis – for the purpose of rating bonds of issuers. Further, subjective judgement seems to play an important role in bond ratings.

Bond rating agencies also take into account factors including the growth rate of an industry and its relationship with the economy, industry risk features, nature of competition, industry structure, competitive strength of the issuing company and their managerial competence.

With reference to financial analysis, in addition to analysis of the level and trend of financial ratios, rating agencies also take into account bond issuer’s earnings capacity and prospects, business risks, financial risks, cash flows, level of protection vis-a-vis the company’s assets, accounting quality and how flexible is the bond issuer financially.

To be included in the Bloomberg Global Investment Grade Corporate Bond Index (a rules-based market-value-weighted index that is focused on measuring the investment-grade, fixed rate, global corporate bond market), a bond must have a minimum par amount of US$ 250 million.

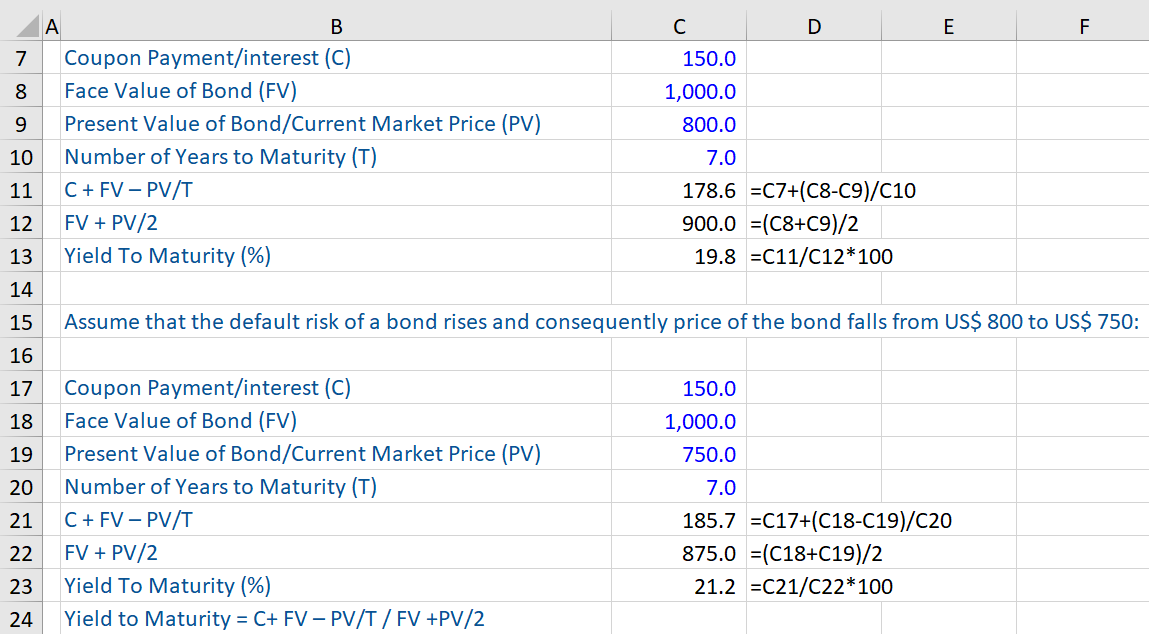

Yield to Maturity, Bond Price and Default Risk

The Yield to Maturity (YTM) is the rate of return (%) from holding a bond to maturity (for example 20 years) – assuming no default and all payments are made as promised by the bond issuer.

A workout of the calculation of the yield to maturity (%) has been given below. Further, when a bond becomes more subject to default risk, then its price falls. Consequently, the bond’s yield to maturity increases i.e. rises.

In the workout below, we assume that Company A’s bond is an investment grade bond with a coupon rate of 15%. After a while, it is downgraded to speculative grade (i.e. the bond has become more subject to default risk). As a result, the price of the bond falls. Therefore, its YTM rises from 19.8% to 21.2% (refer to the workout).