Financial Accounting Excel Template

Sign up to access your free download and get new article notifications, exclusive offers and more.

Featured Course

Financial Accounting

September 15, 2025

What is Financial Accounting?

Financial accounting is the recording and reporting of a company’s financial transactions. These activities are presented in reports that provide an insight into a company’s operations and financial position.

Businesses report their performance on a regular basis, often driven by market or jurisdiction practices and regulations. It is vital for analysts to have a thorough understanding of the financial statements in order to undertake effective investment analysis.

Key Learning Points

- Financial accounting is the process of recording and reporting a company’s business transactions

- For most countries, it is a legal requirement for companies to report their activities in annual reports which consist of the three key financial statements: income statement, balance sheet and cash flow statement (the majority report under IFRS or US GAAP guidelines)

- There are many beneficiaries and users of financial statements including but not exclusive to investors, creditors, employees, government authorities and third-party institutions

- Annual reports (or 10-K for US companies) include a large amount of information covering the strategy, business model, goals, financial reports and supporting information of a business

Financial Accounting Standards

For the majority of countries, it is a requirement that companies report their financial statements on a regular basis. How they must report their financial data will vary from country to country, but most will follow one of two frameworks.

IFRS vs. US GAAP

These are the two accounting standards that company reports will generally fall under:

- US Generally Accepted Accounting Principles (US GAAP)

- International Financial Reporting Standards (IFRS)

Each framework provide a list of rules and guidelines to help companies prepare their financial statement. These are based on four main accounting principles:

- Consistency: calculations are completed consistently period on period

- Going concern: the business will continue for the foreseeable future

- Accruals: revenues and expenses are recognized as incurred

- Offsetting: items are not netted off unless required by rules

Most businesses produce audited financial statements once a year with periodic announcements throughout. Within the US, the annual reports are called 10Ks and the quarterlies are 10Qs. Outside the US, the yearly reports are normally annual reports with the periodic ones being referred to as interim reports.

The primary beneficiaries of these reports include shareholders, investors, creditors and lenders. It is essential the reports are prepared according to one of the two frameworks to fairly reflect the financial results and condition of the company.

Components of Financial Statements

Most businesses comprise of many individual legal entities which are part of the “family” of business or group. The financial reports cover all members of the family and are normally referred to as consolidated accounts.

The financial statements are essentially tables which provide a record of an organization’s activities and financial position.

Financial Statement Key Sections

Financial statements are generally made up of the following key sections:

Three Key Statements

The income statement, balance sheet and cash flow statement are known as the three “key” statements. These outline the company’s total income and expenses across a period, its resources and financial obligations at a specified point in time, and the company’s net cash flow. A strong understanding of financial statements and their content will be second nature to an effective analyst.

Statement of Shareholder’s Equity

Companies also provide a Statement of Shareholder’s Equity which reports the changes in the value of shareholders’ equity or ownership interest in a company from the beginning of an accounting period to the end of it.

Statement of Comprehensive Income

Finally, a Statement of Comprehensive Income represents a company’s change in equity during a specific period from transactions and events that are typically non-cash gains and losses.

Financial accounting involves the preparation of financial statements to provide information about the financial position, performance, and cash flows of a business. Here are some examples which can be found on Felix:

Income Statement

This statement shows the company’s revenues and expenses during a specific period, resulting in a net profit or loss. This is an extract from Coca-Cola’s 2024 10k (or annual report).

Source: Felix

The blue and white striped format is distinctive for US filings. Headings are provided on the left and are typically tailored for the company providing the information. The most recent year’s financial performance is displayed along with prior years.

Balance Sheet

This provides a snapshot of the company’s assets, liabilities, and equity at a specific point in time. It must always balance, meaning assets equal liabilities plus equity. This report is dated December 31st, which is the last day of Coca-Cola’s 2024 fiscal year.

The balance sheet will report current (or most liquid) assets at the top of its asset list, with non-current items appearing below. The liabilities are ordering in a similar way, with short-term liabilities at the top and shareholder’s equity below.

Source: Felix

Learn more about balance sheet items and download the free Financial Edge template. This excel download contains line items which need categorizing into assets, liabilities and shareholders’ equity and shows how to create a balance sheet containing the information.

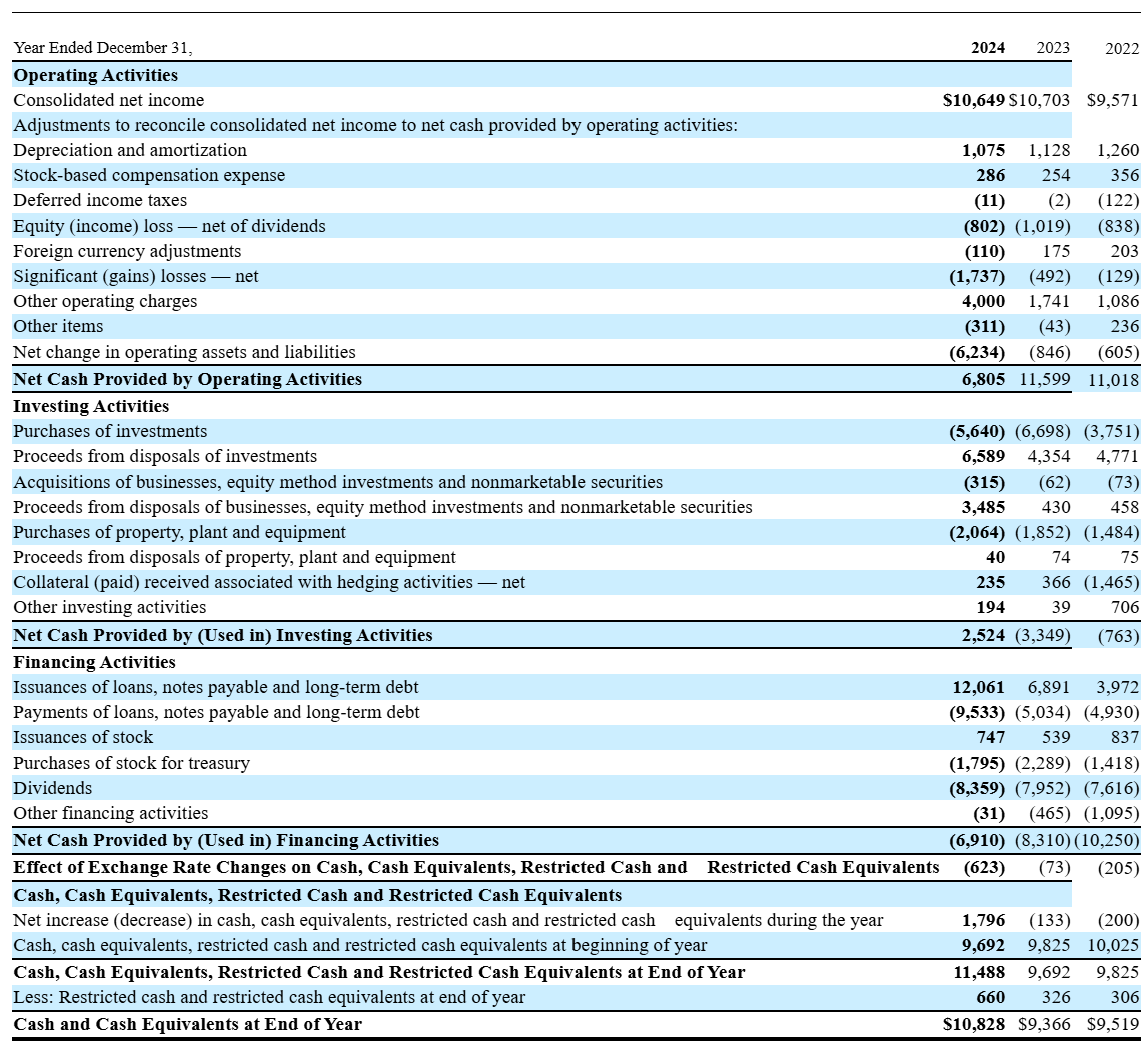

Cash Flow Statement

These financial reports show the cash generated and used during a specific period. This is divided into three sections: operating, investing, and financing activities. These sections can be seen in Coca-Cola’s statement showing how the cash has moved through the business during the fiscal year.

Source: Felix

Analysts will look closely at the cash flow of a company to ensure that the core operations (cash flow from operations) are generating a healthy amount of cash. This can then be used to fund investment, such as capex projects (cash flow from investing) as well as service any debt, loans or other obligations within the company (cash flow from financing). Finally, it will show the cash at the beginning and end of the period, and how much has moved during the fiscal year.

Management, Discussion and Analysis (MD&A)

In addition to the financial statements, there is also some commentary provided by the company on its performance during the fiscal period. The management discussion and analysis (MD&A) is produced by the management of the company and addresses the business successes and performance within the prevailing market conditions.

The report outlines the reasons for the company’s performance, whether this is positive or negative. Often the report presents the company in a favorable light as it’s effectively from those running the company. This may be a slightly biased view but is still very useful for providing further information to analysts. Management will include both qualitative and quantitative assessments of the company, market conditions as well as future plans and outlook.

Analysts will look closely at what management highlights as the strengths of the company in this commentary. What is also important is to understand which, usually less impressive parts, have been carefully omitted. Often management will also guide on market conditions during the period, such as customer habits, currency moves, or pricing, which can all be very helpful with analyzing and creating forecasts for future years.

Financial Statement Footnotes

The footnotes are the final section of the report and provide supporting calculations and additional detail to the statements. Footnotes can be formed of many pages and are a goldmine of data and include the company’s accounting policies.

Annual Report

Public companies present their financial statements as part of an annual report, which contains a lot more information than just the financials themselves. The financial statements tend to be somewhere towards the middle of the annual report.

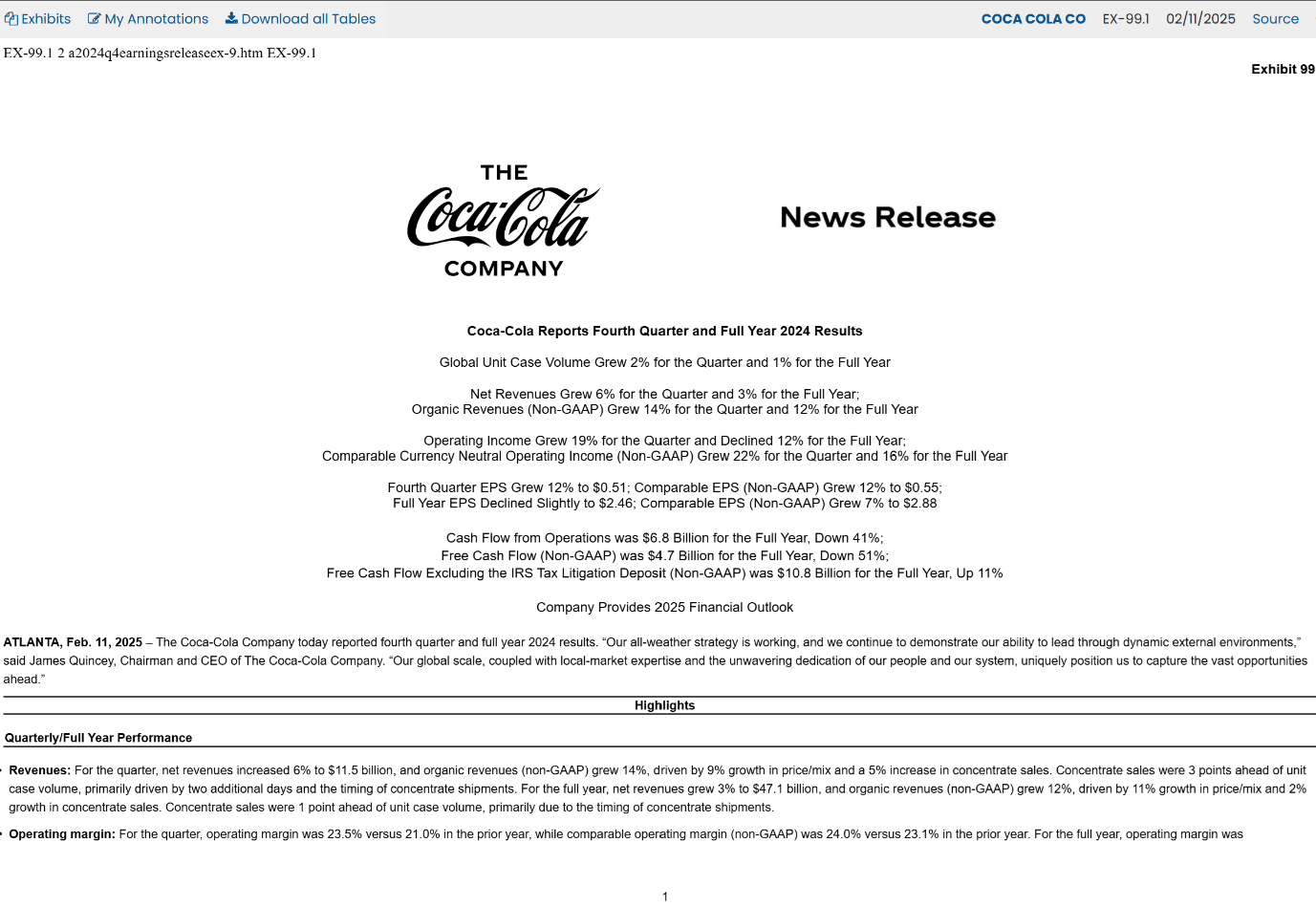

Coca Cola Press Release

In addition, listed companies also issue a press release together with their financial statements. This is a very useful source of information for an analyst as it provides a summary of the results, highlights key performance metrics, and contains key points from management’s discussion and analysis. It usually contains a reconciliation of the reported profit numbers with an adjusted profit number that management views as being more reflective of recurring performance.

Source: Felix

This is Coca-Cola’s press release to accompany the 2024 full year results being released. The headline commentary notes the volume and revenue changes for the year as well as operating income and EPS for both Q4 and the full year.

Importantly it also provides the 2025 financial outlook for the company, which will likely contain growth targets for revenues and income and well as noting any headwinds facing the company.

The Importance of Financial Accounting

Understanding the fundamentals of these reports is essential when reviewing a company. Professionals from an array of industries will need to understand what these reports show and how to read them. The ability to read and analyze reports is vital to building a successful career in the finance industry.

Financial Accounting vs. Bookkeeping

This table highlights the key differences between financial accounting and bookkeeping, illustrating their distinct roles and functions within the financial management of a business.

| Aspect | Financial Accounting | Bookkeeping |

| Purpose | Prepares financial statements for external users | Systematic recording of financial transactions |

| Scope | Encompasses income statement, balance sheet, cash flow statement | Limited to recording daily transactions (sales, purchases, etc.) |

| Users | External parties (shareholders, investors, lenders, government agencies) | Internal parties (management) |

| Reporting | Produces periodic financial reports (annual, quarterly) | Continuous recording of transactions |

| Standardization | Follows standardized accounting principles (IFRS, US GAAP) | Does not follow standardized principles |

| Analysis | Involves analysis and interpretation of financial data | Focuses on accurate record-keeping |

| Decision-Making | Aids in decision-making for external parties | Provides data for internal decision-making |

| Complexity | More complex, involves preparation and analysis of statements | Less complex, involves recording and organizing transactions |

Conclusion

Financial accounting is a critical process that involves recording and reporting a company’s business transactions. It ensures that businesses can provide accurate and comprehensive financial reports, which are essential for effective analysis and decision-making.

By adhering to standardized frameworks like IFRS and US GAAP, companies can maintain consistency, transparency, and reliability in their financial statements. Understanding these principles is vital for professionals in the finance industry, as it enables them to analyze financial data accurately and make informed decisions that drive business success.