Exercisable

January 5, 2021

What is Exercising an Option?

Employee stock options (ESOs) are widely used by firms to reward and retain their key executives. Unlike regular shares, employee stock options are a derivative contract that gives the option holders (in this case, the executives) a right to trade a fixed quantity of company’s shares after a specified future date at a price fixed today. A company may grant stock options, but they do not have any value until they become exercisable. Once they are exercisable, the options holders have the right to convert their options.

Option holders are only likely to exercise their holding of options if they are in the money. This is the case when the market price of the security is above its strike or exercise price. If the options are out of the money or underwater this is the opposite, and it is unlikely the holder would convert them to shares. This principle is important when calculating the number of diluted shares outstanding as dilution is only anticipated for securities that are “in the money”. This assumes that the holder would not exercise their right for securities that fall below their strike price to avoid capital losses.

Key Learning Points

- Stock options are a form of compensation given to employees

- When an option is “exercisable”, the option holder has the right to exercise them (convert them to shares)

- When an option’s strike price is above the current share price, the option is said to be “in the money”

- There is usually a vesting period of at least 3 years before the options can be exercised, this is a clause to stop the employee leaving the firm

- If an employee has been granted options and they choose to leave the company before the vesting period then they must surrender their options

- Diluted shares outstanding include all the dilutive instruments even if they are not yet exercisable

Options Exercisable Explained

Let us say a company gives an executive 2,000 stock options. These options vest 20.0% every year over 5 years with a total term of 10 years. The exercise price is $10.00.

Here, the total term indicates the expiration period of the options. Vesting refers to earning the right to exercise stock options.

At the end of the first year, 400 options will become exercisable.

The option holder has a choice to exercise these options and sell them. Let us say the stock price of the company is $15. The employee is optimistic about the stock price going up even more in the future, and does not exercise the option.

Next year, a further 20% or 400 options will become exercisable. At this point, the number of options exercisable is 800.

Role of Options Exercisable in Valuation

In valuation, analysts need the number of diluted shares outstanding to arrive at the market equity value and the enterprise value of a business. Options outstanding is a vital element when calculating the diluted shares outstanding. Even though they are not exercised, options exercisable are included in the options outstanding. Why? If the company is acquired tomorrow, all options (exercisable and even those not exercisable) are instantly allowed to be exercised. So, the dilutive effect of all options needs to be included.

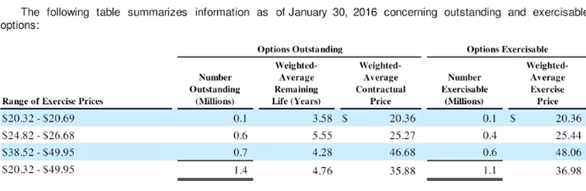

Following is a screenshot of the options outstanding of Gamestop Corporation.

In the above example, the options outstanding (1.4 million) include the options exercisable (1.1 million.) There are different ranges of exercise prices. In the first range ($20.32 – $20.69), all the options have become exercisable. However, in the second and third categories, some have not become exercisable yet. Nevertheless, these options exercisable are included in the total number of options outstanding.

Ways to Exercise Options

Cash Purchase:

In this method, the options holder pays the purchase cost and other exercise costs, such as taxes, commissions, etc. Let us say an employee has 100 options exercisable worth $5, and the stock is trading at $10. The employee needs to pay $500 and other expenses to get 100 shares worth $10. Once the employee receives the 100 shares, they can choose to hold/sell some or all of them.

Cashless Purchase:

Here the options holders do not have to pay anything out of their pocket. They have two options, whether to hold the shares or sell all the shares. If the option holder wants to hold the shares, they can sell some shares to cover the exercise cost. In the example above, let us assume the exercise cost is $100. The employee can sell 10 shares to cover the exercise cost and hold the remaining 90 shares. If the employee wants to sell all the shares, they will get $900 in cash (after deducting exercise costs of $100.)